From UK, BIS vaults to Indian shores: Why RBI wants to keep more & more gold at home

")

Your grandparents and parents may have often told you to buy gold to tide over any financial crisis – but, guess what? Central banks around the world are doing exactly that! India ranks among the top 10 countries with highest gold reserves – and its gold reserves have been growing. Not only that, the Reserve Bank of India (RBI) is also choosing to store most of the country’s gold reserves domestically, bringing back several tonnes from abroad.Between October 2025 to March 2026, RBI has brought home 104.2 metric tonnes of gold. RBI had already repatriated around 280 tonnes of gold from 2023 to 2025, which includes 64 tonnes brought back in mid-2025 and around 100 tonnes that were repatriated from the UK.In a world that has seen multiple economic shocks from the pandemic, Russia-Ukraine war, Donald Trump’s tariffs, economies have become more vigilant about their external buffers. Foreign exchange reserves act as an important cushion that defines an economy’s ability to repay its debts. Gold has always been a part of foreign exchange reserves – but its importance is changing – and fast!Central banks around the world have been buying gold, and the trend is likely to continue despite rising prices of the yellow metal. According to the latest World Gold Council report on gold trends, central bank buying is expected to be solid at levels close to those in 2025. Initial estimates of central bank net buying in the first quarter are reassuringly robust, particularly in light of recent price volatility and notable mobilisation of reserves, it says.So why is gold suddenly the go to bet for central banks around the world, including the RBI? And why is RBI choosing to suddenly store a majority of it in the country? Let’s dive in:

Why are central banks, including RBI, buying so much gold?

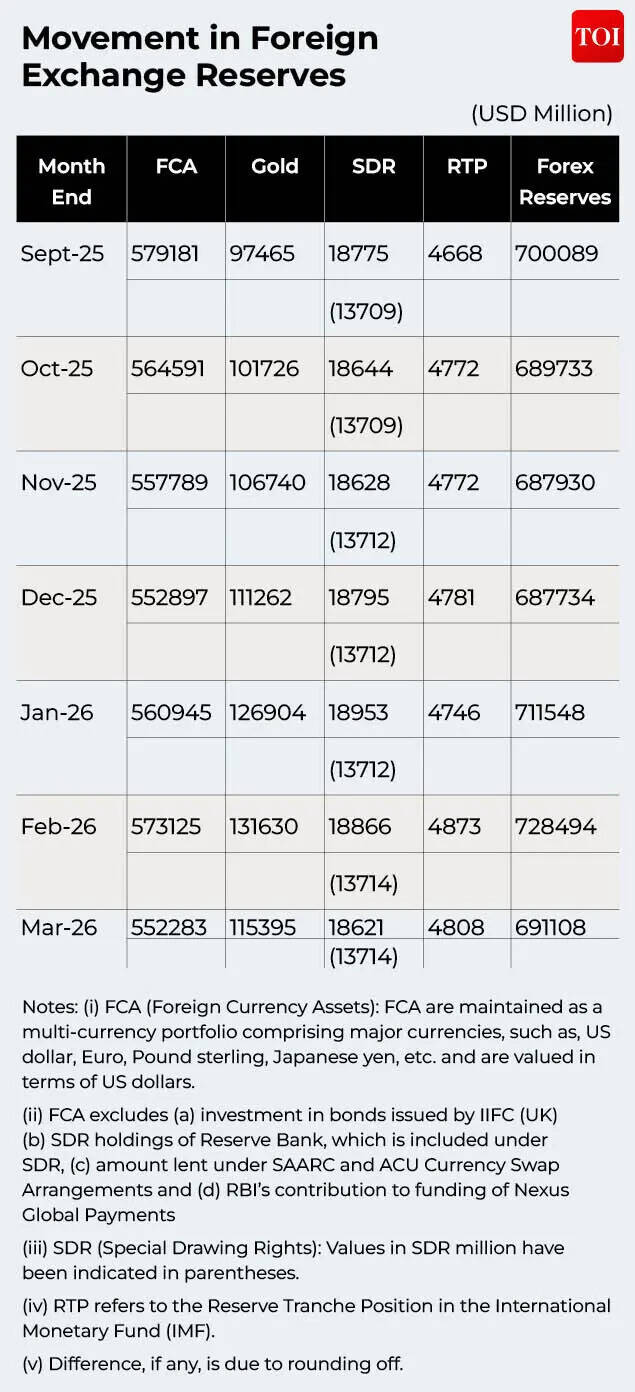

As a recent Assocham report says: Central banks hold gold as part of their official foreign exchange reserves, making them among the world’s largest buyers and holders of the precious metal. Their decisions play a pivotal role in shaping gold prices, influencing market sentiment and impacting the long term dynamics of the global monetary system. The primary reason for central banks to hold gold is to diversify their reserves to safeguard value over long periods. Unlike fiat money, gold’s value is not tied to the economic performance of any single country.A multitude of factors are working in the yellow metal’s favour – it’s a safe haven in times of uncertainty, a diversifier that helps keep the basket balanced, and in the last few years a hedge against the ongoing de-dollarisation that the world is witnessing. Experts have pointed out that central banks have stepped up gold buying as countries are looking to reduce their excessive dependence on the US dollar. Yet another factor that is driving gold purchases is the fear of sanctions in case of geopolitical tensions.The broader de-dollarisation trend has picked up since the Russia-Ukraine conflict and the increasing uncertainty on trade and tariffs that have prompted major countries and emerging markets like China, and India to stock up more gold as a part of the forex reserves mix.What works in gold’s favour is its neutrality – the safe haven asset is not linked to the monetary system of any single country. Hence, global currency volatility, need for hedge against inflation, and sanctions-related asset freeze have prompted gold to be treated as a reliable asset for long-term store of value.In 2024 in particular, India ranked among the top buyers of gold with an addition of 72.60 tonnes to its reserves, second only to Poland which saw an increase of 89.54 tonnes. China, too, has been adding to its gold reserves, consistently ranking among the top five buyers in the last few years.In fact the percentage of gold held by India as a part of its foreign exchange reserves has seen a big jump in the last few years. In FY 2020-21, gold made up just 5.9% of India’s forex reserves. Come 2025-26, it contributes a big 16.7%, which in part is due to rising gold prices, but majorly due to rising gold holdings. In value terms, the share of gold in the total foreign exchange reserves increased from 13.92% at the end of September 2025 to about 16.70% as at March 2026 end.

RBI brings home gold – but why?

The fact that is most notable is that the central bank has not only increased its holdings of gold, but it is also choosing to bring back the physical gold from overseas facilities to store it domestically. In the last few years, this pattern has particularly stood out.As per the latest RBI bulletin, at the end of March 2026, the central bank held 880.52 metric tonnes of gold, of which 680.05 metric tonnes were held domestically. While 197.67 metric tonnes of gold were kept in custody with the Bank of England and the Bank for International Settlements (BIS), 2.80 metric tonnes were held in the form of gold deposits. India has progressively brought back its gold reserves kept outside of India. In March 2023, around 38% of India’s gold reserves were held domestically. This has now increased to about 77% by March 2026.Storing gold domestically is seen to have several advantages – from cost to security, it serves many purposes. Experts note that bringing gold reserves back home reduces a country’s vulnerability to external ad-hocism. India will also save on the costs associated with holding gold reserves abroad.

There are many benefits of doing it which include greater financial sovereignty, risk diversification & economic security as a hedge against crises. Central banks also repatriate gold reserves due to geopolitical risks like asset freezes seen in Russia sanctions, reducing storage costs, and enhancing sovereign control over assets. The issue became particularly relevant when the US decided to freeze assets of Russia after the Ukraine war started.Madan Sabnavis, Chief Economist, Bank of Baroda explains the benefits of bringing back gold reserves. “A central bank would like to repatriate gold assets once it has the structures to house them within the country. The benefits are that there is easy access to these reserves whenever required. Such a measure also does away with counter party risk that arises when lodged in another country,” he tells TOI.The move also serves as a signal of strength for investors. “Bringing back gold is a strong messaging system to inform investors that the country and economy are strong and more importantly mature. This has been done by some developed countries too of late besides India. This also reduces the cost for a central bank as storing in say the UK involves the cost of vaults as also regular audits that have to be done for valuation,” Sabnavis says.

“It also shows less dependence on other countries like the US and UK which are the two major centres that provide such vaulting facilities. In fact, centres like Singapore and Dubai have emerged for providing such facilities given the strength of the bullion trading markets,” he adds.Sachchidanand Shukla – Group Chief Economist at Larsen & Toubro also says that the move is a sign of economic strength.“Repatriation helps in better reserve management. It enables direct custody and flexibility in volatile markets, strengthening financial stability against shocks. Also,it boosts investor confidence by signaling proactive risk management and economic self-reliance,” he tells TOI.To him, this shift signals broader erosion of trust in offshore assets, promoting gold’s role in a multipolar monetary system. Gold repatriation implicitly reflects de-dollarization trends and geopolitical fragmentation, as central banks hedge against sanctions and dollar dominance post-Russia events.Then there is also the currency factor: Gold held domestically gives underlying strength to a country’s currency where it is known that there are large reserves including those held in the form of gold backing the currency. DK Srivastava, Chief Policy Advisor, EY India tells TOI that this has been a trend for BRICS countries where major BRICS+ members have increased their gold reserves by buying it from the international market and by bringing it back from other countries particularly from the western countries to within the domestic jurisdictions. “If and when a BRICS currency is launched, holding relatively larger gold reserves would provide a good initial position to India amongst the BRICS countries. Investor confidence is positively affected when it is known that a country is not vulnerable to external ad-hoc interventions. There is a tangible restructuring of the international monetary and financial system as the world economic system moves from unilateral to a multilateral structure,” he says.In fact, DK Srivastava believes that India should keep all its gold reserves domestically. “Strategically, it makes no sense for a large country like India to keep its gold reserves outside of India. We were forced in the early 1990s to shift some gold reserves abroad in order to avail of an IMF loan at that time. However, it is best to bring all gold reserves belonging to India back to India,” Srivastava tells India.The EY expert says it is a strategic risk to keep gold reserves outside of India particularly in view of the ad-hoc initiatives of the major western countries to freeze financial and other reserve assets if a country follows policies that are not aligned with their interests. “It is best to mitigate this risk for India by bringing the gold reserves back into India to be kept in the RBI vaults,” he says.RBI is not alone in repatriating its gold reserves. Several central banks like France’s Banque de France, Germany’s Deutsche Bundesbank, Serbia’s National Bank have done the same. Repatriation of gold reserves aims to bolster sovereignty and also do away with any foreign custody risks.It is clear that in times of emerging geopolitical uncertainties, where countries are taking unilateral calls to economically cripple others, India is looking to secure its foreign exchange reserves buffer and reduce dependency in a multi-polar world – bringing back its gold is just one step in that direction.